TPD is Big Business!

Here's all the companies you need to know!

8th November 2024

The recent advances in our understanding of TPD and broader induced-proximity concepts has fuelled an explosion in interest in commercialising these ideas across many areas but what is the current shape of the biotech landscape in this area? I keep an informal tracker of TPD-related companies and have mentioned there are “probably about 90” TPD companies so in this post I look a little deeper at this rapidly evolving ecosystem.

When I started working in TPD back in 2012, the competitive landscape analysis was pretty simple: There were essentially no companies focused in this space. No-one was really very interested, after all PROTACs were just weird molecules while we hadn’t really figured out all the details of the glue mechanisms of the IMiDs so the broader applicability here was unclear too. Proteasome inhibitors were the shining examples of drugs harnessing cellular protein homeostasis mechanisms.

Things started to change as biotechs started to pop up in the space. First Arvinas (in 2013), then Kymera & C4 (2015) as well as a few established biotechs also pivoting efforts into the area and soon a trickle turned into a steady stream. In no time the competitive intelligence slide in my decks was getting crowded then overcrowded until today we are running at around 80-90 “TPDCos”.

Most of the early companies focused on TPD via glues or PROTACs though more recently, I’ve also started to add other biotechs also using induced proximity for other applications (protein stabilisation, relocalisation, activation, targeting – though I don’t include more classical bispecific antibody plays). I don’t include big pharma (who are all active in this space, many doing great work), biotechs with a TPD project tucked away in their wider portfolio, or CROs. (See the note at end for more info on how I put the list together)

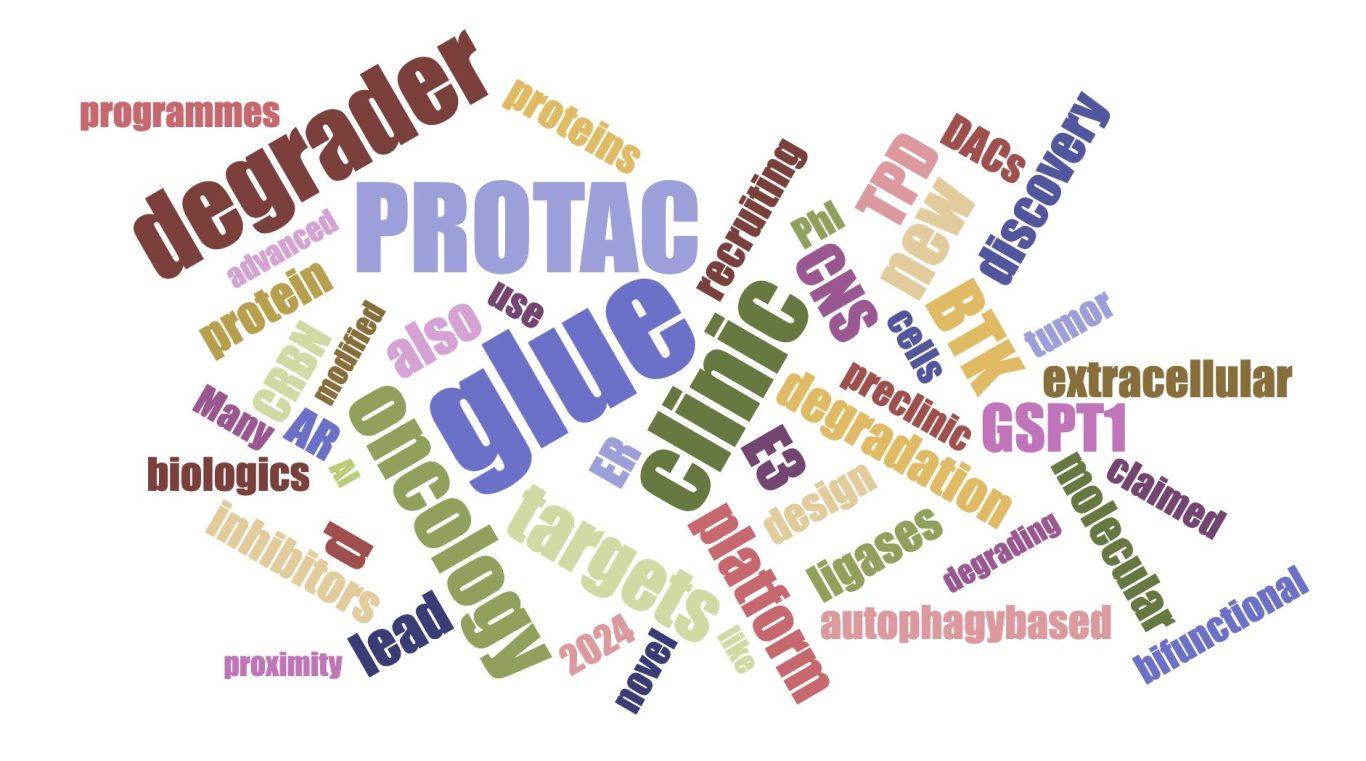

You can see the list of all the companies on my TPDCo Directory page and a clue to the common themes in the wider database from the Wordcloud above. However, to save you visiting nearly 90 company websites, here’s a few interesting headline pieces of analysis which fall out of my take on the landscape.

In total, I currently track 87 TPDCo’s, a figure which increases every few weeks. I know of others still in deep stealth and there are of course many that I don’t know about so the total is likely to hit 100 sometime in mid-2025. Of the 87, six are still very stealthy with little public information to give clues how they plan to differentiate themselves in the space. Oerth Bio is also an outlier as they are focused on crop science rather than human health so if we leave these few aside, we’re left with 80 where I have a decent feel what they’re up to.

Disclaimer – what’s written on a biotech website can often be more aspirational than what has been delivered and is not always a true reflection of current reality (sorry if this is new news to anyone - be wary if you see statements saying “we hope to…” etc) but, hey, I’m happy to take things at face value … as long as data to back up the claims are forthcoming at some point.

Very pleasingly, 21 of the TDPCos are now clinical phase, a number I expect to increase quickly given the number of projects in IND-enabling studies according to website pipelines. This is a great conversion rate from pre-clinical to clinical for a new drug modality given the median company foundation dates are likely in the 2018-2020 window. Many of the clinical projects are exciting first in class though there is an expanding fast-follower, best in class cohort also – imitation is the sincerest form of flattery after all.

Looking at the modality being used, over 90% of companies trade mainly on small molecule agents though 16% use biologics (or RNA-encoded proteins). Some companies use both. An increasing number have also expanded into degrader-antibody conjugates (an area it is well worth investing in if you have very potent degraders), blurring these figures somewhat.

Within those small molecule outfits, 60% mainly use bifunctional agents – most commonly PROTACs but now an increasing number of other-TACs also. 44% also claim glue discovery platforms, a number which has increased significantly over the last year or so I’d say.

It can be difficult to assess exactly what ligases or other effectors companies are using but, based on target selection, patents etc, you can see that almost half are clearly still firmly in the CRBN and/or VHL space – there’s a lot of opportunity here of course and certainly for glues, CRBN is by far the E3 with the most knowledge. However, over 40% claim to be working on effectors which are not VHL or CRBN.

Platforms based on “novel E3s” need to show me the data of potent degradation of non-BRD4 targets before I get too excited but I hope there’s a few new effectors out there to give us some variety. There’s also deubiquitinases, FKBP, biologic targets, tumor markers and many other effectors of course which can work well – I estimate that at least 10 of the companies are using induced-proximity with non-degrading goals in mind.

Now, I’m not saying my database is the best or the most comprehensive out there (please let me know of any updates I need to make) – many of the established competitive intel companies have offerings in this space if you have plenty of money to spend but I contend that mine may be the best value for money (given it is free). I have a lot more insight and perspectives on the TPDCos in my list – give me a call if you want to discuss anything further.

It's also worth noting that the TPDCo list is not always destined to get longer and longer. There has been some M&A activity (as noted in the table) though perhaps not as much as may have been expected – there are reasons for that we could explore in another post. Many biotechs ultimately fail and you would have seen the likes of Civetta, Cedilla, Polyprox, Celeris and Siduma on previous versions of my list but, alas, they are no longer with us. This is of course desirable – we need to take risks in new areas of science and a healthy failure rate reflects an appropriate amount if risk-taking. Indeed, maybe the failure rate should be higher - a number of the companies on my list have been rather light on newsflow or funding announcements recently so we may see a few companies dropping off in 2025 also.

I am optimistic that the first FDA approval of the latest generation of TPD medicines could come as soon as 2025 but also that the collective TPD pipelines across the industry are in good health to produce a steady ongoing stream of new medicines to allow the cool science of TPD to directly benefit patients across many areas – and to help us understand the best places to apply TPD therapies and how to get them to approval as quickly as we can.

Historically, not all great science has turned into great medicines but, with TPD, I’m confident we’re firmly on track to deliver.

Footnote - some quick comments on how I view the TPDCo landscape:

The real fast movers & innovators in this space are largely the biotechs whose main or only focus is advancing a therapeutic pipeline of TPD agents as they tend to be most motivated to make new things work and take risks. So it’s these TPD biotechs I focus on. I know of course that most, if not all, big pharma have active TPD efforts across many areas but this is part of a much larger portfolio so I don’t include them in my analysis. Many biotechs are also now dipping their toe in the TPD waters with perhaps one or two degrader projects in their larger portfolios but this is more of a reflection of how TPD has now become part of the mainstream repertoire of drug discovery strategies so I don’t try to include these.

Likewise, there are many specialist CROs which provide outstanding services, some of them focused in TPD offerings, but again, I don’t include them in my list otherwise it would get very long indeed and somewhat less focused – it’s those companies trying to advance their own programmes into the clinic which best characterise the vibrancy of the field.

I acknowledge that my list is somewhat subjective and almost certainly not 100% accurate with companies emerging from stealth or pivoting in or out of TPD all the time but I hope it is useful. However, if you see errors or feel your own company should be added, please let me know using the link below or at enquiries@janusdrugdiscovery.com and I’d be happy to make appropriate updates.

Note also, I am not advocating or recommending the work of any of these companies but rather simply trying to keep track and understand the shifting trends in this exciting area of life science business.

© 2023-2024

All rights reserved. Janus Drug Discovery Consulting Ltd

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.